Email: Keith@KeithDeJohn.com

Phone: (714) 612-5501

Email: Keith@KeithDeJohn.com

Phone: (714) 612-5501

Low Rates. No Hassle.

Find out how Keith De John can help make qualifying for a low rate mortgage EASY.

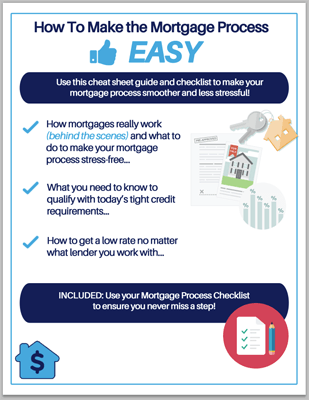

Get your FREE copy of my Cheat Sheet and Checklist...

"MORTGAGES MADE EASY..."

"How to Qualify For a Low Rate Mortgage without the Headaches, Hassles, or Haggling!"

I'm Keith, and I'm Here To Help

Would you like to discuss your mortgage with me?

All consultations are NO CHARGE and NO OBLIGATION.

What I Do

Outstanding Communication and Follow-up

We keep you informed and return all emails and calls promptly so that you never have to wonder what is going on with your loan.

Professional Support

Count on us to be there with you and to help you navigate the entire mortgage process. We'll help you cut through the red tape and avoid the common mistakes people make.

Competitive Low Rates

We work with you to find the right program and secure low market rates to make sure you are paying the lowest payment each month.

Close Your Loan On Time

Not all lenders can close quickly or on time. We work closely with you through the process to meet all deadlines and make sure that your loan closes on time.

Who I Help

First Time Home Buyers

We know how overwhelming the process of buying a home is, especially if it is the first time that you're doing it. We will work closely with you to explain the process, to protect you from making mistakes that could cost you later, and to ensure that your mortgage gets approved and you get the home that you are so excited to be buying!

Refinancing Home Owners

If you already own your home but you are looking to refinance to either save money with a lower interest rate or possibly take some cash out for any reason, we can help you with that. We also can show you how to make sure you are structuring your new financing to get the best deal possible.

Investment Buyers

If you're buying real estate for investment purposes, we can help you secure low rate financing to maximize your ROI.

Seniors Seeking Reverse Mortgages

If you are 62 years or older and are looking for options to stay in your home without a mortgage payment or to access your home's equity while still living there, I can answer your questions about reverse mortgages so you can decide if they are right for you.

Where To Find Me

CUSTOM JAVASCRIPT / HTML

Work With Me

I recognize that your needs are unique, and I would love to find out exactly how I can be of service to you.

Contact me by email or give me a call.

EMAIL ME

If email is your preferred method of contact, go ahead and email me.

CALL ME

Call me today with any questions you have about the process - I'm happy to help.

Stay Connected

Keith De John, NMLS # 252519

CA DRE #00948234

CA DRE #00948234

Mortgage Specialist

1805 E. Garry Avenue

Santa Ana, CA 92705

Arbor Financial Group

NMLS #236669

CA DRE #01845041

NMLS Consumer Access

© Copyright All Rights Reserved | Terms & Conditions | Privacy Policy

Website Design by OriginatorSuccess, Hammer Solutions, LLC